Don't Leave Equity for A Term Deposit

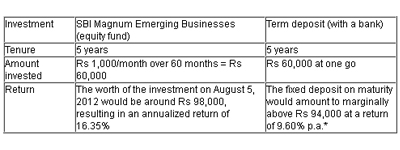

*According to data provided by the Reserve Bank of India (RBI), term deposit rates of major banks for more than 1-year maturity in July 2007 were in the range of 7.50–9.60 percent. We went with the highest rate.

*According to data provided by the Reserve Bank of India (RBI), term deposit rates of major banks for more than 1-year maturity in July 2007 were in the range of 7.50–9.60 percent. We went with the highest rate.

The Investment In Equity Gained Over All Fronts. Why?

Though the amount invested in both cases was  60,000, the investment in the fund scored because you did not have to put down that amount at one go. There was no strain on your finances. Instead, you disciplined yourself into investing every month over 60 months! In the case of the fixed deposit, you had to part with that much of cash at one instance.

60,000, the investment in the fund scored because you did not have to put down that amount at one go. There was no strain on your finances. Instead, you disciplined yourself into investing every month over 60 months! In the case of the fixed deposit, you had to part with that much of cash at one instance.

On maturity, you do not have to pay any long-term capital gains tax on your mutual fund investment if you hold the units for a year before selling. In the case of the term deposit, you would be taxed according to the income bracket you fall under. If you fall in the highest tax bracket of 30 percent, out of the interest you earn in the above illustration, a little more than 10,000 would go in taxes.

No matter the turmoil the equity market faces, in the end investments in good businesses will deliver. If you invest and stay grounded in a good equity fund (note, the catch here is to invest wisely, not blindly), you stand to win over the long term. Despite a term deposit giving the impression of a safe haven, it will turn out to be a losing proposition once you take taxes and inflation into account.

: Ushering In A New Era Of Ai-Driven Cybersecurity")