Magazine :

Magazine :

Why Savings is Not a Replacement for Term Insurance

In terms of financial planning, protecting our loved one's safety and well-being in the event of unforeseen circumstances is one of the most important considerations. The value of insurance becomes apparent in this situation. Although many people are aware of how important having insurance is, there is a common misperception that term insurance can be replaced by savings alone. In this blog, we will debunk this myth and explore why savings is not a sufficient substitute for term insurance and both should go hand in hand.

Savings as a Foundation:

Savings play a vital role in financial planning, offering numerous benefits. They provide a readily accessible pool of funds for emergencies, such as medical expenses or sudden job loss. Moreover, savings can be utilized for short-term goals like vacations or purchasing a new vehicle. By regularly setting aside a portion of their income, individuals can gradually accumulate wealth and achieve their desired financial milestones.

The Limitations of Savings as a Financial Safety Net:

While savings offer immediate liquidity and flexibility, they may fall short of providing long-term financial protection. Unforeseen events like disability, critical illness, or premature death can significantly impact a family's financial stability. In such cases, relying solely on savings can quickly deplete the funds, leaving loved ones vulnerable. This is where term insurance steps in to bridge the gap.

Understanding Term Insurance:

Term insurance is a type of life insurance that provides coverage for a specified period, typically ranging from 10 to 30 years. It offers a death benefit to the beneficiaries if the insured person passes away during the policy term. Unlike savings, term insurance acts as a financial safety net for your loved ones, ensuring that they are protected from potential financial hardships in the event of your untimely demise.

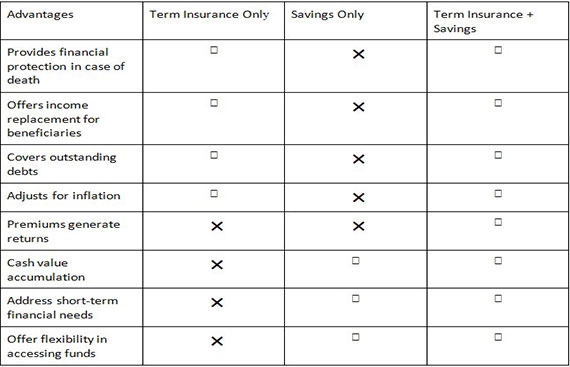

- Income Replacement: One of the primary reasons savings alone cannot replace term insurance is the aspect of income replacement. For most families, the loss of the primary breadwinner can have devastating consequences on their financial stability. While savings can help cover immediate expenses, they may not be enough to replace the income generated by the deceased individual over an extended period. Term insurance provides a sum assured to the beneficiaries, helping them maintain their standard of living and meet ongoing financial commitments, such as mortgage payments, education expenses, and daily living expenses.

- Debt Repayment: Another vital consideration when evaluating the role of savings versus term insurance is the management of outstanding debts. In today's society, it is common for individuals to have various liabilities, such as mortgages, car loans, or personal loans. In the unfortunate event of the insured's death, these debts do not disappear. They can burden the surviving family members, creating a significant financial strain. Term insurance can provide the necessary funds to repay these debts, ensuring that financial obligations do not burden or deplete the savings intended for other purposes.

- Affordability and Peace of Mind: One of the misconceptions about term insurance is that it is an expensive form of coverage. On the contrary, term insurance is often more affordable than other types of life insurance, such as whole life insurance or universal life policies. By paying a relatively low premium, individuals can secure substantial coverage for a specific period, providing peace of mind to both the insured and their beneficiaries. Savings alone may not offer the same level of security and peace of mind that term insurance can provide.

- Inflation: The value of savings can erode over time due to inflation. Term insurance policies often have a benefit amount that is not fixed, but rather adjusted for inflation. This ensures that the coverage amount keeps pace with the rising cost of living, providing adequate protection for the family's financial needs.

- Long-Term Financial Goals: Savings alone may not be sufficient to meet long-term financial goals, such as funding higher education for children or enjoying a comfortable retirement. By combining savings with term insurance, individuals can protect their savings and ensure that these goals can still be achieved, even in the event of an untimely death.

- Financial Stability: Building a substantial savings fund takes time and discipline. However, relying solely on savings for financial security can leave a family vulnerable. Term insurance complements savings by providing immediate financial stability and protection, especially during critical periods when savings might not be enough.

By combining savings and term insurance, individuals can create a robust financial safety net that addresses the limitations of savings alone. This approach provides a balanced strategy, ensuring both immediate protection and long-term financial goals are met, offering greater peace of mind and security for the family.

Evaluating the Value of Term Insurance:

Using a term insurance calculator can help individuals evaluate the value of term insurance in their financial planning. By comparing the estimated premium costs against their savings, individuals can gain a realistic perspective on the affordability of term insurance and recognize its essential role in securing their family's financial future.

Conclusion:

While saving money is undoubtedly an integral part of financial planning, it should not be viewed as a substitute for term insurance. Savings alone cannot provide the same level of financial security and protection that term insurance offers to your loved ones. Income replacement, debt repayment, and the ability to fulfill future financial goals are crucial aspects that term insurance addresses comprehensively.

By combining both savings and the best term insurance plan that caters to your needs, individuals can create a robust financial plan that ensures the well-being and financial stability of their families in the face of adversity. It is essential to consult with a qualified insurance professional to understand your specific needs and determine the optimal combination of savings and term insurance to protect your loved ones; future.

Remember, when it comes to securing your family's financial well-being, it is always better to be safe than sorry.

Read More News :

Chandrayaan 3 success is a testament of our deep tech capabilities: MoS IT

Government to launch 'Mera Bill Mera Adhikar' scheme to encourage customers to ask for bills