Should I claim Input Tax Credit as per GSTR-2A or GSTR-2B? March 2021 Update

Input Tax Credit is one of the dearests of all the GST domains.

ITC is important to keep the cash-flow in proper order and to make the capital available for the business processes.

Though ITC is a lucrative feature, it is sometimes tricky.

Taxpayers have always found themselves stuck in riddles, such as the way to avail ITC and the reconciliation important for claiming this Input Tax Credit.

In this article, we shall be discussing a recent clarification issued by the Central Board of Indirect Taxes and Customs.

You will get to know if the ITC has to be availed as per your GSTR-2A or GSTR-2B.

We will go through this article in 3 parts:

- Understanding GSTR-2A and GSTR-2B

- Rule 36 (4) of CGST Act, 2017

- CBIC’s recent clarification

What are GSTR-2A & GSTR-2B?

‘Tell me and I’ll forget; show me and I may remember; involve me and I’ll understand.’

Staying true to the above maxim, let me explain this with a very easy-to-understand example rather than going into the detailed explanation of these two terms.

Here the Recipient is buying a service from the Supplier-zoo zoo.

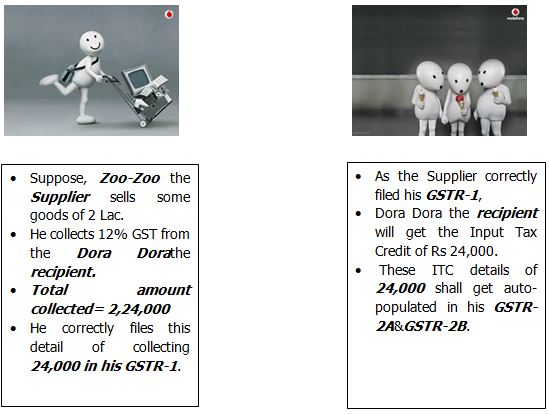

Now, as a ‘Supplier’ which return shall zoo-zoo file?

- He shall file GSTR-1 for all the services or goods or both which he has sold to the recipient.

- GSTR-1 also popularly called 'Outward Supplies Details' will be filed by the 11th of the subsequent month.

How will the Supplier’s GSTR-1 affect the Recipient’s ITC details?

- The Supplier has filed his GSTR-1 for the corresponding outward supplies, based on this, the ITC details will get auto-populated in the Recipient’s GSTR-2A.

- Now the same Input Tax Credit details get auto-populated in the new form called GSTR-2B.

Tell me more on GSTR-2B

- GSTR-2B can be generated by the recipient every month based on the GSTR-1 filed by their suppliers.

- It gives you a complete idea about the eligible and ineligible Input Tax Credit for that particular month.

- Generated on the 12th of every month next to the tax period.

- GSTR-2B remains constant for a period, unlike the GSTR-2A.

- GSTR-2B is available for Normal taxpayers, Casual taxpayers as well as the Special Economic Zones (SEZs).

What is Rule 36 Sub-rule 4 of CGST Act, 2017?

The rule is read as,

Input tax credit under GST to be availed by a registered person in respect of invoices or debit notes, the details of which have not been uploaded by the suppliers under sub-section (1) of section 37, shall not exceed 10 % of the eligible credit available in respect of invoices or debit notes the details of which have been uploaded by the suppliers under sub-section (1) of section 37.

Let's continue our above example to understand this quickly.

Now, Dora Dora, the Recipient's GSTR-2A&GSTR-2B will get auto-populated based on the Supplier’s GSTR-1.

So the Recipient now can avail an Input Tax Credit based on his GSTR-2A&GSTR-2B.

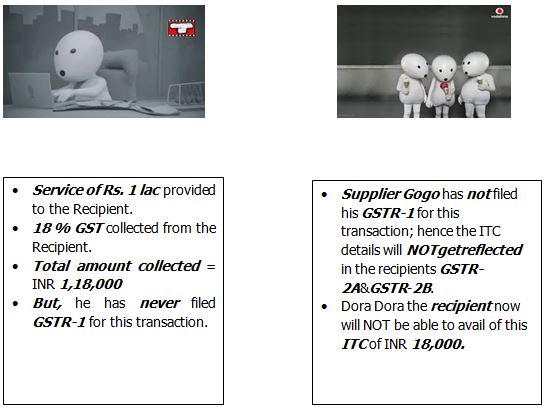

There’s one more Supplier Mr. Gogo from whom Recipient Dora Dora is availing a service worth  1 lac.

1 lac.

Now, when you look at both the examples as a whole, you’ll understand the following things.

What is the eligible ITC of the Recipient Dora Dora as per Books?

- 24,000 + 18,000 = INR 42,000.

But how much ITC is available in GSTR-2A as well as 2B of the Recipient?

- Only INR 24,000.

- As 18,000 is not reflected in 2A&2B of the Recipient.

Now how Input Tax Credit can be availed by the Recipient in his GSTR-3B?

- Here, Rule 36 (4) of the CGST Act, 2017 comes into the picture.

- This rule simply states that,

Maximum Eligible ITC for the Recipient shall be,

Eligible ITC auto-populated in GSTR-2B + 5% of eligible ITC

i.e. the Maximum permissible ITC,Dora Dora the Recipient can take for this month shall be,

24,000 + 5% of 24,000 = 24,000 + 1,200 = INR 25,200

The remaining Input Tax Credit of INR 18,000 can be availed by the Recipient when the defaulting Supplier Gogo will file his GSTR-1.

What is the confusion regarding availing of ITC as per GSTR-2A or GSTR-2B?

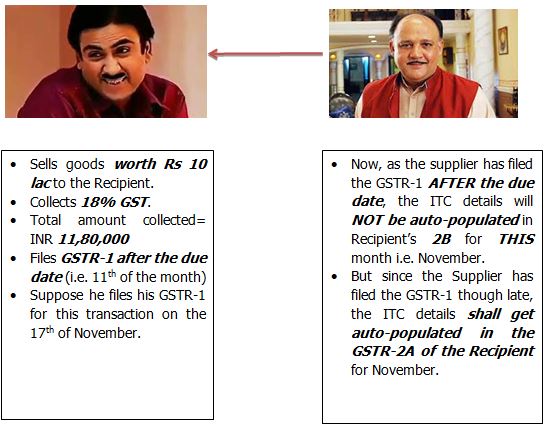

Suppose, a Recipient purchases goods worth INR 10 lac from a Supplier.

Now the problem we can highlight in the above example is that,

In Recipient’s GSTR-2B = ITC of INR 1,80,000 is NOT Available.

In Recipient’s GSTR-2A = ITC of INR 1,80,000 is AVAILABLE.

Now there is confusion among the Recipient, whether he shall avail the ITC in his GSTR-3B as per his GSTR-2A in the current month i.e. November, or should avail the ITC as per his GSTR-2B in the next month i.e. December?

Now, this is what the CBIC has clarified through a tweet recently.

CBIC’s Clarification

The CBIC has clarified this confusion among the taxpayers througha tweet dated March 15th, 2021.

Mind you, there has been no specific circular issued in this regard, but as the tweet comes from the authorised Twitter handle, this information carries a lot of importance.

What are they saying?

The CBIC has clarified that the Input Tax Credit MUST BE AVAILED as per the invoice details available in GSTR-2B.

The invoice details in the GSTR-2A shall not be used to avail of the Input Tax Credit.

Whatever details you have to check in regards to your Input Tax Credit details, you MUST refer to GSTR-2B Reconciliationonly.

Advice to the Taxpayers

All the taxpayers are advised that you should carry out your Input Tax Credit Reconciliation as per GSTR-2B only.

You should prefer the services ofautomated GST software which will minimize your errors and can help you in availing the maximum Input Tax Credit.

Many people are taking incorrect ITC as per the GSTR-2A details and hence are falling into further complications.

Choose automated software & stay updated and compliant with the ever-changing rules of GST.

Until the next time…

Disclaimer :

Images used in the article are for education purpose only. No copyright is intended & all rights are reserved with the respective company.

About the Author– GSTHero– Making GST Simple! GSTHero is the best GST filing, e-Way Bill Generation & E Invoicing Software in India. GSTHero is a government authorized GST Suvidha Provider. Both Businesses and Tax Practitioners can file GSTR 1, GSTR 3B, GSTR 9 and GSTR 9C with all supporting reports. 1 Click Auto Reconciliation& report-matching feature helps you in claiming up to 100% ITC and finds your GST Defaulting Suppliers. GSTR2A vs GSTR-3B, GSTR-1 vs GSTR-3B, ‘GSTR-1, GSTR-2A & GSTR-3B’ annual report matching is also provided by GSTHero.

GSTHero ERP Plugins provide 1 Click e-Way Bill & E-Invoice, Generation, Operation & Printing from your own ERP like Tally, SAP, Marg, Busy, Microsoft Dynamics, Oracle & others itself with high data security