Magazine :

Magazine :

7 FACTORS THAT AFFECT YOUR HEALTH INSURANCE PREMIUMS

Good healthcare is one of the basic needs for everyone, and the rising cost of managing an emergency hospitalization make insuring such costs a necessity. Health insurance, as we know it, helps us to bear any sudden hospitalization expenses. However, the health insurance itself has a cost associated with it in the form of an annual premium.

The premium for the health policy is an important factor to consider while buying health insurance for yourself or your family. However, lowest premiums may not bring you the best plans, and it is advisable that you understand the premiums well before buying.

Here are seven factors that affect the health insurance premiums:

1. Physical and medical risk factors:

Physical and medical risk factors are the basic criteria through which insurers judge the inherent risk of the insured person. The following risk factors are primarily responsible fordetermining the health insurance premium.

• Age: The higher the age, the higher the premiums will be.

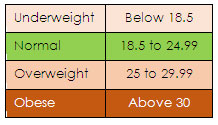

• Body Mass Index (BMI): Body mass index determines the amount of fat accumulated in the proposer’s body. Obese people (or people with higher BMI) are prone to more diseases and considered riskier than people with normal BMI. People with too low BMI are also considered higher risk and will face higher premium charges for their health insurance.

Following is a sample table which defines the BMI index for Indians (as per latest update):

• Any Disability/Handicap:Physical disabilities can occur due to disease or accident. In any case, it can lead to higher risk of suffering from various health issues and thus a higher risk for an insurer.

2. Medical History:

Medical history influences the treatment and diagnosis of the insured person. An insured person with an adverse medical history may develop certain health issues later in life and will be a higher risk to consider. Therefore, even if there is no existing medical condition at the time of purchase your premium may be higher in the following cases:

• Pre-existing Medical Conditions: If you had been treated for a disease earlier in life. Your premiums may be higher depending on the kind of disease it was. Life threatening diseases, even if fully treated, may increase your premium cost for a new health insurance.

• Family Medical History:Certain ailments are hereditary, therefore, if your family’s medical history indicates theexistence of any of the hereditary diseases your premium will be higher for health insurance.

3. Residential and Occupational Hazards:

While medical history and hereditary problems play their part in affecting the health of a person, the surroundings where he/she lives and works, have much to say about his/her health as well. Thus, the following are considered while deciding the premium cost of the health insurance for any person:

• Residential Location: Different regions are divided based on their population and hospital density. The higher the population and hospital density, the lower the premium, as theinsurer, can distribute the total risk among thelarger population and better healthcare facilities. However, there can be exceptions based on claim history as per the region.

• Occupation: Occupation plays a major role in defining the person health. A clerk (or a person with a desk job) is less likely to develop occupation related health issues than a flight pilot. Thus, the riskier the profession, the higher the premium.

4. Marital Status& Gender

Marital status and gender of a person also affect the health insurance premium.A married male is more likely to have a lower premium rate than a married female.Though some insurers like Apollo Munich, simply do not discriminate based on gender and both males and females can be sure to pay identical premiums for the same covers.

5. Sum Insured

The rise in premium payable with the sum insured or the amount of cover available is too obvious. However, the case here is not just that. As you increase the sum inured, insurers may at times add certain features and benefits not available for the lower sum insured covers.

Also, higher sum insured for Mediclaim may not result in equally higher sum assured for critical or accidental insurance riders. Most insurers limit the sum assured allowed under additional covers but offer higher sum insured for base Mediclaim plan.

6. Additional Features

Additional features include higher room rentlimit and higher limits for daily cash and ambulance expenses, and surely, they come at a cost.

7. Additional Covers

Add-on covers and benefits increase your health insurance cost. However, some of the additional benefits may even be necessary. For example, critical illness cover is as important as the basic medical insurance cover for any individual.

Similarly, accidental disability is also a major risk in today’s environment which can adversely affect not just your savings but also future earning capacity.

Thus, you will need to base your purchase decision on the covers and benefits rather than the premium of the health insurance plan. After all, the money you pay now should benefit you and your loved ones in time of need.

.jpg "Gurbinder Singh Punn: Enabling Leaders To Achieve Unencumbered Success Through Effective Coaching")

.jpg "Navigating Success Presenting Innovative Insights")