Know The Many Benefits Of A Critical Illness Cover

Many of usare happily insured against any risk aversion. Hospital expenses are covered under the health insurance policy and; we have a family health plan. We have conveniently presumed; we have done maximum to secure our treatment expenses.What else can an average man do to secure his family’s health? A family medical insurance is a paper-proof of that. It will give you access to the best hospital treatment at an affordable cost.Your income now has an insurance cover.

Figure 1source: http://finvin.in/wp-content/uploads/2012/07/Accident.jpg

However; there is still a reason to worry. Your family health insurance scheme may not be enough. Think again, if the following happens to you.

• You suffer from a heart attack

• Your spouse is diagnosed with breast cancer

Consider this illustration to understand this in a practical context.

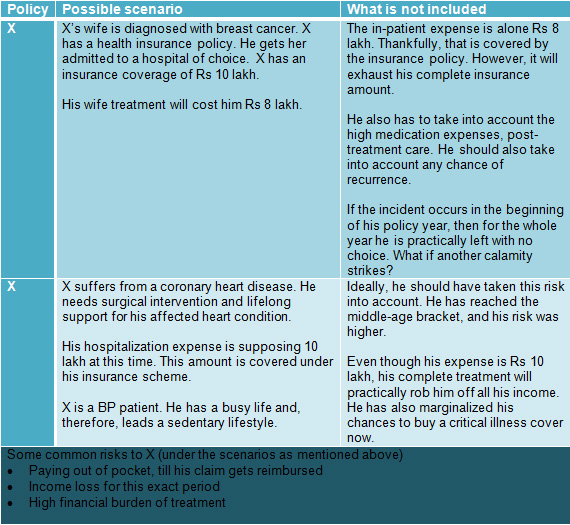

Mr. X has a health insurance cover, a family floater policy. It covers the general health risks, covering his spouse, and parents (one parent is asenior citizen). X is 40 years old.

Why should X buy a critical illness policy?

While a health insurance policy covers hospitalisation expenses, a critical illness cover pays a lump sum amount on diagnosis of a critical ailment. This amount can be used to meet household expenses, recuperation aids and make up for the loss of income due to fall in the ability to earn money. Overall, a critical insurance policy acts as a supplement to your existing health insurance portfolio.

What is covered under a critical illness policy?

The number of critical ailments covered under the policy may vary from one insurer to the other. Most insurance companies cover 8 to 20 critical illnesses or even more. Some of the diseases which are covered under the policy are cancer, coronary artery bypass, kidney failure, heart attack, major organ transplant, paralysis, etc.

How much coverage is sufficient?

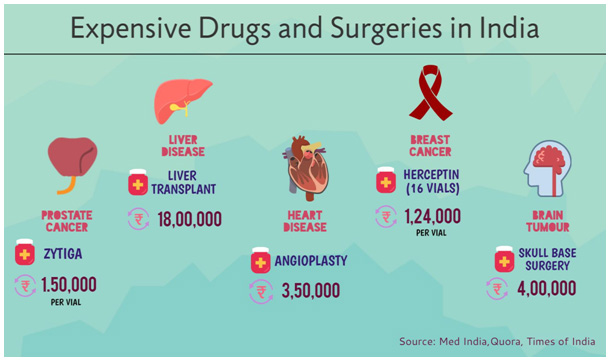

The cost of critical ailment treatment would typically run in lakhs, and one may have to either take the help of relatives or dig into their existing savings. In addition to this, contracting a critical ailment hampers an individual’s earning capacity as well.

One should have a sufficient critical illness coverage which should be decided on the basis of various factors like family history, annual income, age, etc.

Conclusion

Critical illness cover is an imperative health cover, and it should be present in an individual’s portfolio to get complete protection againstunforeseen events. So, the strategy to follow is that buy a comprehensive health insurance policy and then add critical illness policy to get comprehensive cover.