January - 2010 - issue > Business

VAS Trends Changing Dynamics of the Game Top 5 Current VAS Transitions in India & Emerging Markets

Tarun Handa

Sunday, January 3, 2010

Today Entertainment category of VAS contributes the highest share in any Indian operators VAS portfolio. Bollywood today is the world’s largest entertainment industry, producing more than a 1000 movies a year with an audience of more than 2 billion viewers across 127 countries and the content demand is not only high in India but also overseas. Interestingly today’s mobile devices have shifted the entertainment from a content or network play to a device based play. Mobile devices with integrated music and video player, FM and high memory features have flooded the market accompanied with low cost associated with it. Entertainment content from the web world is being fed into the device memory and is being used. Even games for this case are downloaded from the web and dumped into devices.

In such an unfavorable scenario, the Operators are making a lot of investments in infotainment content and services. The demand for infotainment content and services like news, astrology, location based services, maps etc; have had a significant growth in the recent past and is expected to grow even more in future.

2. Focusing on Rural VAS

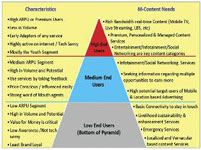

In emerging markets especially in countries like India, majority of the population is rural i.e. the Bottom of the Pyramid (BoP). Rural teledensity in India was at 16.54 percent as of May 2009 compared to urban teledensity of more than 88.6 percent around the same period. This figure is expected to reach about 36.25 percent by 2013.

Around 30 percent of Airtel’s wireless subscriber base resides in the rural parts of the country, whereas for Vodafone, BSNL, Reliance Communications and Idea Cellular, the rural user base is around 31 percent, 34 percent, 19 percent and 30 percent of their respective wireless pie. With such mass revenue potential hanging around, operators are shifting their focus on VAS for BoP. Initiatives by Airtel, Reliance and Idea Cellular to connect with their rural masses are already visible with their tie ups with livelihood content providers like IFFCO and Reuters Market Light for services related to agriculture, weather and livelihood. The below figure clearly maps out the characteristics of the different mobile population and their mobile content needs.

However, finding localized content for the BoP mobile population remains a food for thought for the operator. Though many content providers are emerging in this value chain that can help with rural and livelihood related content, monetizing the content will require quite a bit of effort from the operator in terms of creating awareness and delivering true value addition.

3. Subscription to On Demand VAS (Sachet)

To give mobile users flexibility, especially the ones at BoP with Value Added Services, many operators have begun offering services like ringtones, alerts and games on a daily pricing model instead of monthly. Reliance Communications rolled out this model in June 2009, however, impact on its VAS revenues has not been known. In 2006 RCOM tested out the ’sachet model’ in association with Jump Games, now a Reliance Entertainment company - it effectively reduced the price points as other operators were either offering subscriptions or bundling VAS. Many of us would believe that with lower price points the VAS ARPU would also be low but this type of packaging will help VAS become a larger part of the subscriber pie thus increasing the penetration. Moreover this would give an on - demand user experience that makes the consumer feel more connected to its operator.

The above figure depicts the price sensitiveness of Mobile Content / VAS in a developed market like U.S. where majority of the mobile population own a high end device. This gives us a picture that if developed countries like U.S. with loaded gadgets and infrastructure are so price sensitive then what would be the scenario in emerging markets where majority of the population is at the BoP.

4. SMS based to Voice based VAS

Voice based VAS services constitute around 40% of the total VAS market today and most of them are via IVR which is expensive to the operator as well as to the end user. Voice based VAS services are expected to grow roughly at a CAGR of around 80% in next 3 to 4 years. In geography like India where there are more than 1600 regional dialects and 22 constitutionally approved languages, it becomes difficult for operators to deliver text based services in vernacular.

Moreover Voice based services do not have any learning curve for the end user as compared to an SMS or a GPRS based service where the end user has to learn the process of using or accessing the services. And with majority of the population not tech savvy, this would act as a barrier to penetration and usage of mobile services as voice has the highest user experience level. Adjacent figure clearly depicts that only eight percent users are GPRS users and 49 percent are SMS of which maximum is P2P.

The below figure is an outcome of a survey conducted by Ericsson on the control factors affecting use of m-content services in Uganda and India. The major barriers identified for access to mobile services in India were high cost of the service followed by awareness on how to use the services and its unavailability in local languages. Today, an end user pays Rs 6/min for an IVR based service like listening to songs, setting CRBT, etc. which is way too expensive and is a major barrier for mass usage of VAS.

Thus, in order to increase usage of services and to reach wider audiences, operators need to focus on Voice delivery, but they also need to work around innovatively on the high IVR costs associated with current Voice based services.

5. Increasing usage of Mobile Internet

With mobile phones becoming the fastest penetrating digital device and perhaps the most popular one, it has also become the easiest way to access any information on the fly. With internet boom in India a decade ago, we were right in believing that the world had shrunk and information on anything in any part of the world is just a click away. Yet the broadband rates, PC penetration, power supply and the last mile connectivity are key issues to be addressed for mass adoption of broadband.

Mobile adoption on the other hand has been phenomenal and with falling handset prices and enhanced features, it has enabled internet access to the masses. Though speeds are a challenge which we are sure 3G and forthcoming technologies will address to, but mobile has made the shrunk world more personalized because though PC stands for personal computer, it’s never personal. An average town family that has one PC has more than one mobile. In rural areas, where even mobile is a shared device, this helps in accessing information as the last mile connectivity and cost of devices are not a challenge in contrast to a PC.

According to TRAI’s March 2009 report, there are about 117.82 million mobile Internet users out of 415 million mobile users in India in contrast to 6.4 million broadband PC Internet connections. India had 101.1 million mobile subscribers owning phones capable of accessing Internet at the end of December 2008. VAS – Getting the ABC Right

For a VAS service to succeed in any market there are three basic key attributes that must be looked at. These are as follows: 1. Accessibility of Service 2. Bundling of Service 3. Content Quality

A killer VAS is a combination of all these above attributes. Any standalone attribute cannot contribute to the success of a VAS. The users will not subscribe for a VAS that has poor or unauthorized content, or will not subscribe the VAS in spite of good content if the packaging or pricing is too high or the delivery channel for accessing the service has a complicated learning curve. Ensuring the fulfillment of ABC attributes is just half the job done. Supplementing ABC with the key marketing essentials like promotion, branding and lifecycle management completes icing on the cake. It is very important for a VAS to effectively communicate its value delivery to its target audience failing which the VAS is unable to connect with revenues that it can deliver. Success of a VAS also depends upon management of its lifecycle. VAS like CRBT would have not seen a boost if boosters like Press * to copy the song, Gaana Bolo Hello Tune Pao, etc; hadn’t been given. Today CRBT constitutes as much as 40 percent of an Indian Operator’s VAS revenue and is an unbeatable killer VAS.

The author is Strategic Account Manager VAS, SDP & Mobility Solutions, Tata Consultancy Services

More articles from this issue