Why alternative lending is the next big thing in loans

For the last couple of years, alternative lending is on a roll winning more clients from traditional banks by day. For those first hearing this term, alternative lending is a wide array of institutions that provide all kinds of credit products but aren’t traditional banks. Peer-to-peer lenders, in-house financing, SME lenders, community banks, etc. The most common selling points of an alternative lending operation are that the loans from those companies are easier to get, the interest rates are lower, and the overall experience is smoother. But let’s dig into the specifics of why alternative lending is so on the rise now.

Faster development of the technology

Alternative lending grows alongside FinTech. And FinTech companies specialize at creating innovative solutions that solve problems in the niche of finances. So let’s take a regular alternative lending operation as an example. To function, it needs loan origination software, solutions for underwriting, collateral management, borrower evaluation, risk management, debt collection, loan servicing, reporting, supervision, and regulatory compliance. Lucky for the alternative lenders, companies like TurnKey Lender work tirelessly to make all those processes fully automated. And unlike banks which are busy concentrating on selling and servicing their products and services, FinTech companies are fully focused on creating and developing software.

Full automation of the processes

Alternative lenders strive for full automation of the whole lending process. This means that the client doesn’t have to go to a brick-and-mortar branch, they don’t need to stand in queues and wait for several days after the documents are submitted. Because when a machine does the analysis, makes credit decisions, and takes care of servicing, it takes minutes if not seconds where it used to take days. Which brings me to my next point.

Quicker services and products

Due to the automation of the majority of tasks, lenders need far less resources to run their operations and for the end user, it becomes much easier to work with them. You just log in, go through a simple onboarding process, get evaluated and get issued a loan. That’s of course only true if your alternative lender is using the right lending automation software.

Improved user experience

If you’re a lender, you want your users to have an enjoyable experience working with your business. You want to have intuitive flows within your lending platform, you want to have all the needed integrations in place and the design should be consistent across your whole online presence. And even though that takes some work, if you’re using the right platform to automate your lending needs, that shouldn’t be a problem at all. So all you have to take care of is a decent website and marketing.

Better interest rates

Of course, users pay attention to the usability of the system and to how good it works, but the ultimate selling point of a credit product will always be the winning interest rate. Well here’s the good part, alternative lenders can afford themselves to not have brick-and-mortar branches and have drastically smaller staffs than that of banks due to all the automation we’ve been talking about. So, given that their marketing is good enough, they can have a lower interest rate and still work at a profit.

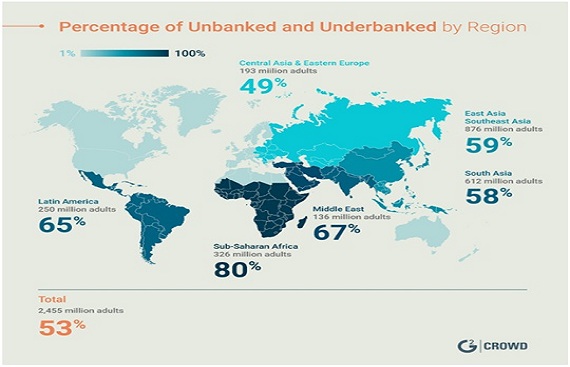

Reaching the underbanked and unbanked

The development of technology and the fact that it becomes more accessible and affordable increases competition. In addition, new algorithms and artificial intelligence can help make better decisions about issuing loans to people who were previously considered ineligible. So the lenders now can look into reaching the enormous market of the 2.5 billion of underbanked and unbanked people, bringing the world of global financial inclusion closer.

Less human error

Alternative lending operations rarely rely on paperwork. They rely on algorithms. And algorithms don’t get tired and don’t lose documents on their tables. So the implementation of an advanced intelligent lending platform into a lending operation significantly reduces the amount of human error which inevitably occurs when people work with people.

Final thoughts

Like any industry, lending is evolving. And even though big banks are a little slow to respond to the changing market forces, they will. And this means that the technology will keep on advancing to meet the ever-growing market need for innovation. For the end users of credit products and for the alternative lenders who are just looking to get into the field it’s great news. Because now it’s easier than ever to get started and launch a successful business in finances.

Read More News:

Appvance Raises $5 Million for Continuing Lead Autonomous Testing