Savings Accounts: More than just a Piggy-bank

Savings accounts are the most basic and essential financial instrument. They also happen to mark our foray into banking and managing personal finances (of course, this part comes a bit later in life). Usually, the first savings account is opened, when we are minors, as a joint account with one of our parents. This is followed by the first salary account, and from there on it becomes a focus point of our financial well-being.

Savings accounts are often viewed solely as an emergency fund or a tool that allows instantaccesstocash. But, they have now evolved beyond just that. Let’s look at what a modern-day savings account offers you today:

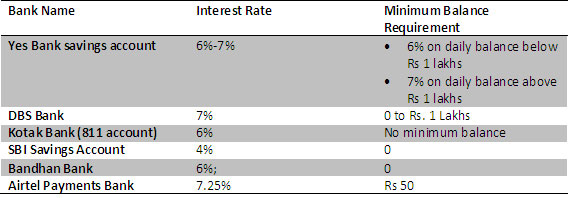

1. Interest rates:Most traditional financial institutions offer a standard rate of interest of 4%, but with the entry of newer banks, customers are benefitting from competitive interest rates. Further, even though interest rates are intrinsically tied to the minimum balance requirement, most new banks are breaking this habit, making it a win-win for us, the customers.

2. Sweep-in facility: One of the latest features of savings accounts is that they don’t let accountholders’ money sit idle in the account. If your deposits exceed a certain threshold, banks automatically transfer these funds into a fixed deposit (FD). With this sweep-in facility, you get to benefit from a higher rate of interest than the one offered by a traditional bank account. If this isn’t enough, you can also customize this facility to your needs. You can determine the balance to be maintained and even the tenure of the FD. For example, with SBI’s Savings Plus Account, you can choose the tenure from 1 year to 5 years. But note, you cannot decide the fixed deposit interest rate as that is fixed by banks. Further, if you need more money than available in the account, funds from your FD can be also swept back into your account.

3. Insurance: Given the uncertainty of life, it’s but natural that our trusted savings account also provide protection against unforeseen difficult circumstances. A lot of banks offer insurance products, such as life and accident cover. For example, HDFC’s SavingsMax Account offers customers accidental hospitalization cover of Rs 1 lakh p.a. and an accidental death cover of Rs 10 lakhs. Similarly, even Canara Bank offers accountholders life insurance cover of Rs 1 lakh. Apart from this, some banks also offer insurance on debit cards, for protection against loss and misuse.

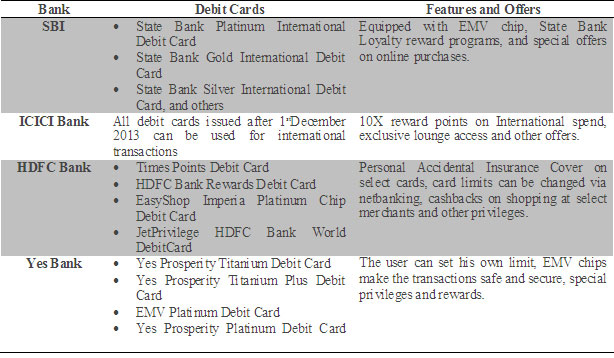

4. Debit cards and Rewards: Debit cards provide on-the-go access to your savings account, while also rewarding you every time you swipe them at point-of-sale (POS) terminals. Banks are now also offering international debit cards that can be used overseas for making transactions or withdrawing cash free of cost.

5. Demat account: If you are an avid investor, you can sync your savings account with demat and other trading accounts free of cost. By doing do, you can conduct transaction seamlessly without any hassles. What’s more you can do this effortlessly on the web and across devices (both Android and iOS). For example, if you open a SBI savings account, you can also access the financial markets via SBI Cap Securities, which will hold your demat account and online trading accounts. The same applies to Yes Bank, HDFC Bank and other banks which convert your savings account into a 3-in-1 account, allowing you to invest in equity, derivatives, currency and mutual funds through the humble the savings account.

6. Linked accounts:If you and your family happen to hold your individual accounts with a single bank, you now have the option to club them all under one umbrella and benefit from “Family Savings account” option. One of the biggest benefits of grouping multiple accounts is how the minimum balance requirement can easily be met. For example, four family members have an account each in a bank where the minimum monthly balance requirement is of Rs 25,000. In this case, together all four would have to store Rs 1 lakh. But by grouping the four accounts, they would need to maintain a total of Rs 25,000 only, without inviting any penalty on the account.

7. Locker facility:Most banks offer a safety deposit box or locker when you open a savings account with them. However, this depends on the type of account and the minimum average quarterly balance one is supposed to maintain. Another important point to note here is that the locker fee depends on the location of your bank branch (rural or urban) and the size of the locker. The below tables show

|

Federal Bank Experience Centre Locker Fees |

||||

|

Locker Dimensions |

Annual |

Quarterly |

Monthly |

Key Deposit |

|

A 125x175x492 |

3600 |

900 |

300 |

15000 |

|

2A 125x352x492 |

7200 |

1800 |

600 |

25000 |

|

D 189x263x492 |

8400 |

2100 |

700 |

30000 |

|

4A 278x352x492 |

9600 |

2400 |

800 |

35000 |

|

2D 189x529x492 |

12000 |

3000 |

1000 |

40000 |

|

4D 404x529x492 |

24000 |

5100 |

1700 |

50000 |

To sum up, it’s safe to say savings accounts have come of age and reinvented themselves to stay relevant and ahead of the curve in today’s tech-dependent era. Whether you open a bank account in a public sector bank or private, you stand to benefit from all the above listed features and more. So, whether it’s an SBI savings account linked with SBI fixed deposit or an account with HDFC Bank, offering 3-in-1 banking feature, your savings account will take care of all your needs. From saving for a rainy day to being an investment instrument, savings accounts have come full circle.

: Ushering In A New Era Of Ai-Driven Cybersecurity")