ET Brings Already Shortlisted Health plans for Older Couples

BENGALURU: Today, there are as many as 24 companies in general insurance and life insurers offering various types and sizes of covers. This introduces a pain in choosing a suitable product for a specific life stage requirement which can offer the best value for your money. Additionally, the interpretation of terms and conditions, limits, and sub-limits is so confusing and one hardly has time to go through it.

The health care and medical treatments are always at a premium, and the health insurance plans are crucial for all; especially to those who have had a very good experience of life. It’s a good time to take knowledge of the best offerings in the health sector and ensure an independent future for them. For their convenience, ET has listed the top rivals for its “ET Wealth-PlanCover.com” rankings for couples falling in 41-60 age groups. Here’s the link.

Methodology

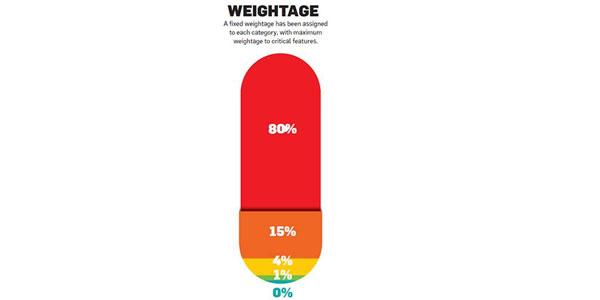

Considering the importance for a given customer segment, most relevant features in health policies have been divided into five categories—Critical, Motivation, Standard, Luxury and Does Not Matter. Factors such as product pricing (charged by the insurer as the policyholder ages) have been taken into account in ranking. The allocation and its individual weightage is based on the data of claims available in public records published by the Insurance Regulatory and Development Authority of India (IRDA), PlanCover.com's analysis of the claims it has handled, and its experience in managing claims.

Critical: Assigned 80 pct weightage

The category includes features having the highest cost implication such as benefits under room rent limit or capping for various treatments. In the case of being low or absent, as a result, you may incur higher mortgage during hospitalization of a patient.

Motivation: Assigned 15 pct weightage

This features incidents for low probability of occurrence for the segment; however, the cost of implication would be high. It is mostly where innovation occurs for targeted marketing of products, say, restore benefits, which work specifically for family floaters. Though the chances of these being used are extremely low, it offers huge relaxation to the consumers.

Standard: Assigned 4 pct weightage

The features with high feasibility but low/minimal cost implication (in overall health care) are being included in here. You can call these as standard features because they are the part of most covers, typically due to the IRDA directives. For example, free-look period, claim intimation/submission, portability, and others.

Luxury: Assigned 1 pct weightage

These are features with a low-cost implication and low eventuality. It includes health check-up benefits, a second medical opinion with another specialist, and more.

Does not matter: Assigned 0 pct weightage

The features are relevant but inessential and hence, can be ignored. Maternity benefits for senior citizens, for e.g.

Read Also:

GST Passage Can Lead To 8Pct GDP Growth Over Next Few Years: Report